Stock Price Prediction using TD3 Reinforcement Learning

DOI:

https://doi.org/10.65521/ijacect.v15i1.1868Keywords:

Abstract

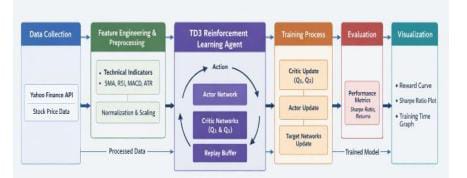

This review examines the application of deep reinforcement learning techniques to algorithmic trading in equity markets, with emphasis on optimizing risk-adjusted returns through intelligent portfolio management. We survey the complete pipeline from data acquisition and feature engineering to agent architecture and performance evaluation. The review focuses on TD3 (Twin Delayed Deep Deterministic Policy Gradients) implementations that learn continuous position control strategies while accounting for realistic market constraints including transaction costs, position sizing, and drawdown management. Key components analyzed include technical indicator selection, custom trading environment design, reward shaping mechanisms, and comprehensive performance metrics beyond simple returns.

Downloads

Published

How to Cite

Issue

Section

License

This work is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.