Equivariant Neural Learning Models for Financial Trend Forecasting

Keywords:

Abstract

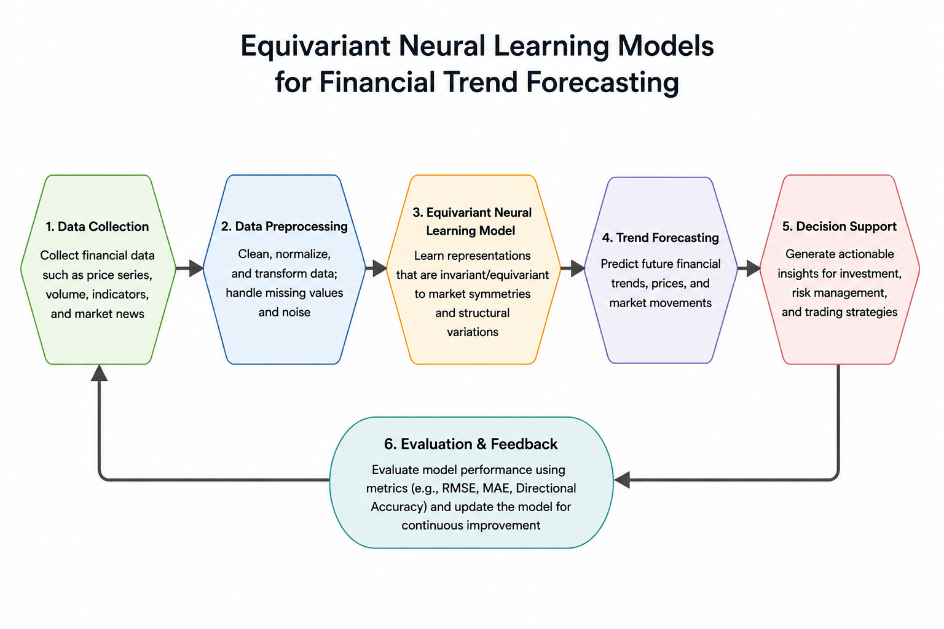

Financial markets exhibit complex, nonlinear, and highly dynamic behaviors, making accurate trend forecasting a challenging task. Traditional statistical models often fail to capture structural invariances and spatial-temporal dependencies present in financial time-series data. This study proposes an Equivariant Neural Learning Model (ENLM) for financial trend forecasting. The framework leverages equivariant neural networks, which preserve transformation consistency under input shifts and structural variations, improving robustness and generalization in volatile financial environments. The model integrates deep learning-based sequence modeling with symmetry-aware feature extraction to enhance predictive accuracy. The proposed system is evaluated on historical financial datasets, and performance is measured using accuracy, RMSE, directional accuracy, and prediction stability. Experimental results demonstrate that equivariant neural models outperform conventional deep learning and statistical forecasting techniques in capturing market trends.