Deformable Graph Intelligence for Financial Market Prediction Using NLP

Keywords:

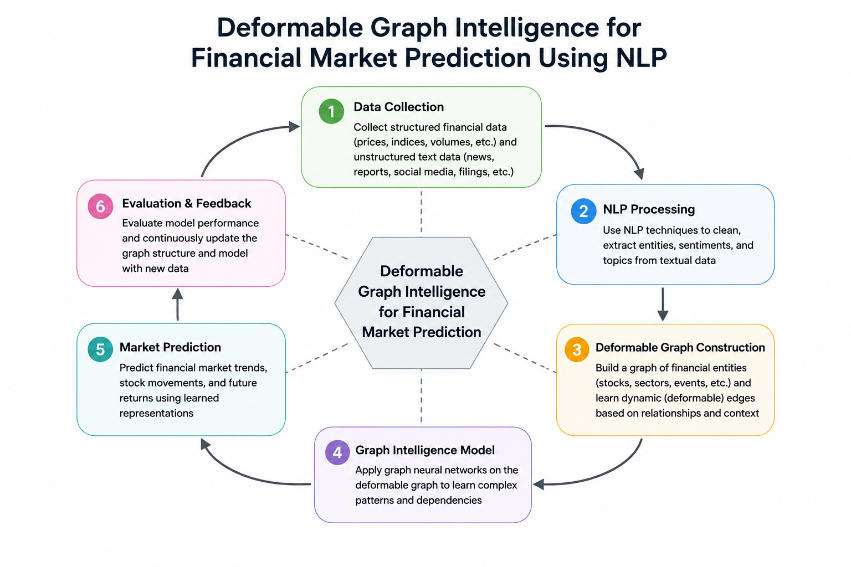

Abstract

Financial markets are highly complex systems influenced by structured relationships between assets and unstructured textual information from news, social media, and financial reports. Traditional forecasting models often fail to effectively integrate relational graph structures with natural language signals. This study proposes a Deformable Graph Intelligence Framework (DGI-NLP) for financial market prediction. The model integrates graph neural networks (GNNs) with natural language processing (NLP) and introduces deformable graph attention mechanisms to dynamically adjust inter-asset relationships based on evolving market sentiment and structural changes. The proposed framework is evaluated on multimodal datasets combining historical price data and financial news sentiment. Performance is measured using prediction accuracy, RMSE, F1-score for trend classification, and robustness under market volatility. Experimental results demonstrate that deformable graph intelligence significantly improves forecasting performance compared to conventional graph-based and NLP-based financial models.