Deep Learning and Optimization Approaches in Risk Prediction in Financial Management of Listed Companies Based on Optimized Deformable Graph Convolutional Networks Under Digital Economy: A Review

DOI:

https://doi.org/10.65521/intjournalrecadvengtech.v14i1.2557Keywords:

Abstract

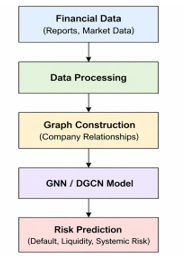

The digital economy has significantly transformed financial systems, increasing the complexity and interconnectedness of risk prediction for listed companies. Traditional statistical models, such as logistic regression and Z-score methods, are limited in handling nonlinear, high-dimensional, and dynamic financial data, leading to the adoption of advanced deep learning techniques. This review focuses on Graph Convolutional Networks (GCNs) and their advanced variant, Deformable Graph Convolutional Networks (DGCNs), for financial risk prediction. DGCNs enhance conventional graph models by introducing adaptive receptive fields, enabling dynamic modeling of evolving relationships among financial entities such as firms, markets, and supply chains. The study also explores optimization strategies, including metaheuristic algorithms, attention mechanisms, and hybrid architectures that combine DGCNs with LSTM, transformers, and autoencoders to capture both structural dependencies and temporal dynamics. Furthermore, the integration of multi-modal data sources, such as financial records, social media sentiment, and regulatory filings, is highlighted as a key advancement for improving predictive accuracy and early risk detection. Empirical findings indicate that optimized DGCN-based models outperform traditional approaches in tasks like credit risk assessment and financial distress prediction. Despite these advancements, challenges related to interpretability, scalability, and regulatory compliance persist, emphasizing the need for more robust and explainable systems.

Downloads

Downloads

Published

How to Cite

Issue

Section

License

This work is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.