Artificial Intelligence Techniques for Deformable Graph Convolutional Networks with NLP Based Social Sentimental Data for Enhanced Stock Price Predictions: Trends and Challenges

DOI:

https://doi.org/10.65521/intjournalrecadvengtech.v14i1.2554Keywords:

Abstract

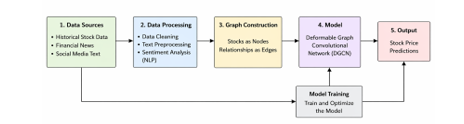

Financial markets are complex, dynamic systems influenced by quantitative indicators, macroeconomic factors, and investor sentiment, making stock price prediction a challenging task. Traditional models such as ARIMA and GARCH often fail to capture nonlinear dependencies and sentiment-driven dynamics present in modern financial environments. The rise of deep learning and graph-based architectures has enabled more effective modeling of temporal and relational patterns in financial data. This paper presents a comprehensive review of advanced artificial intelligence techniques, focusing on the integration of Deformable Graph Convolutional Networks (DGCNs) with Natural Language Processing (NLP)-based sentiment analysis. DGCNs extend traditional graph neural networks by enabling adaptive graph structures that dynamically model evolving inter-stock relationships and complex market dependencies. Simultaneously, transformer-based NLP models such as BERT and FinBERT extract sentiment signals from unstructured data sources including social media, financial news, and analyst reports. These sentiment features are fused with structured financial data to create a multimodal predictive framework that captures both market behavior and investor psychology. The review analyzes datasets, methodologies, and evaluation metrics used across recent studies, demonstrating improved predictive performance of hybrid models. However, challenges such as noisy sentiment data, computational complexity, and concept drift remain significant. This work provides insights into current advancements and future directions for developing robust and intelligent financial forecasting systems.

Downloads

Downloads

Published

How to Cite

Issue

Section

License

This work is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.