A Survey of Methods and Architectures for Deformable Graph Convolutional Networks with NLP Based Social Sentimental Data for Enhanced Stock Price Predictions

Article Sidebar

Main Article Content

Abstract

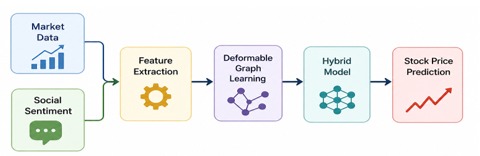

Stock price prediction remains a challenging problem at the intersection of finance, mathematics, and computer science due to the complex, dynamic, and sentiment-driven nature of financial markets. Traditional statistical and machine learning models often fail to capture relational dependencies, temporal dynamics, and behavioral influences embedded in market data. The evolution of deep learning has enabled more sophisticated approaches that integrate multiple data modalities for improved forecasting performance. This paper presents a comprehensive review of a tri-modal framework combining Deformable Graph Convolutional Networks (DGCNs), Natural Language Processing (NLP)-based sentiment analysis, and dynamic graph construction for stock price prediction. Graph convolutional networks model the relational structure of financial markets, while their deformable variants introduce adaptive mechanisms to capture evolving inter-asset relationships more effectively. Simultaneously, transformer-based NLP models such as BERT and FinBERT extract sentiment signals from unstructured data sources including social media, financial news, and earnings reports. These sentiment features are integrated with structured financial data to form a multimodal predictive system that reflects both quantitative trends and investor behavior. Empirical studies demonstrate improved accuracy and robustness over traditional and single-modality models. However, challenges such as data preprocessing, noise handling, and scalability remain. This review highlights key advancements and future directions for developing intelligent, robust, and scalable financial forecasting systems.