AI Based Equity Portfolio Management System

DOI:

https://doi.org/10.65521/ijacte.v15i2S.2988Keywords:

Abstract

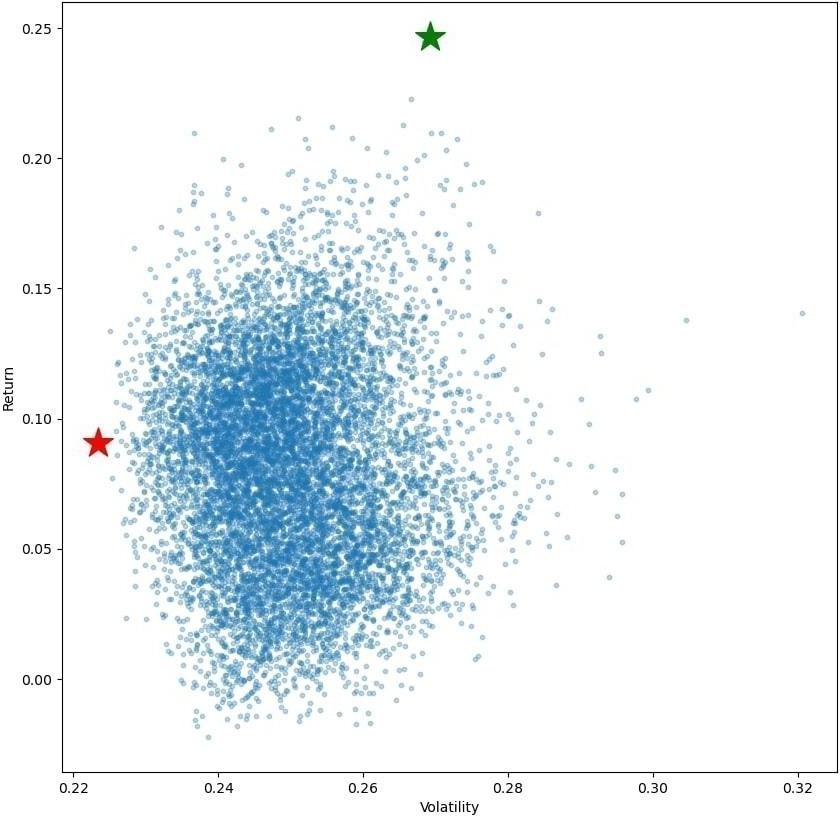

Portfolio optimization is a fundamental challenge in financial decision-making, especially in dynamic and volatile markets such as the Indian stock market. Investors often struggle to construct portfolios that balance risk and return effectively due to fluctuating market conditions, sector-specific variations, and unpredictable economic factors. This study presents a structured and data-driven approach for designing optimized equity portfolios across thirteen major sectors listed on the National Stock Exchange (NSE) of India. Using historical stock price data from 2017 to 2021, the research explores three widely recognized portfolio construction methodologies: the Equal Weight Portfolio (EWP), the Minimum Risk Portfolio (MRP), and the Mean- Variance or Optimum Risk Portfolio (ORP). Each method employs mathematical and statistical techniques to evaluate daily returns, annual volatility, covariance, and correlation matrices, enabling a comprehensive understanding of risk- return dynamics. The study incorporates the top ten stocks from each sector based on free-float market capitalization, making the analysis both sector- specific and representative of real market conditions. These portfolios are then evaluated on actual stock performance data from the year 2022 to determine their practical effectiveness under real- world market fluctuations. Such a two-phase evaluation—training on historical data and testing on real unseen data.