Optimized Deformable Graph Convolutional Networks for Financial Risk Prediction in Digital Economy

Keywords:

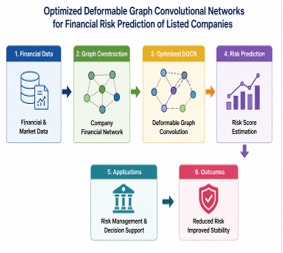

Abstract

The rapid expansion of the digital economy has significantly transformed financial systems, increasing the complexity of risk prediction for listed companies. Traditional statistical models, such as logistic regression and rule-based approaches, are inadequate for handling high-dimensional, nonlinear, and temporally dynamic financial data. The interconnected nature of modern financial ecosystems further necessitates advanced models capable of capturing relational dependencies and evolving risk patterns. This paper reviews graph-based deep learning approaches, with a particular focus on Deformable Graph Convolutional Networks (DGCNs). Unlike standard graph models, DGCNs introduce adaptive receptive fields that dynamically adjust neighborhood relationships, enabling more accurate representation of heterogeneous financial networks. The study also examines optimization techniques such as attention mechanisms, temporal modeling with LSTM and TCN, multi-scale feature extraction, and hyperparameter optimization to enhance predictive performance and robustness. Applications of these models span financial distress prediction, credit risk assessment, fraud detection, and systemic risk analysis across global datasets. Empirical findings demonstrate that DGCN-based approaches outperform traditional and baseline methods in accuracy and generalization. Despite these advancements, challenges remain in interpretability, scalability, and regulatory compliance, highlighting the need for future research in explainable and efficient financial risk prediction systems.