AI-Based Risk Forecasting in Financial Management of Publicly Listed Companies: Trends and Challenges

Keywords:

Abstract

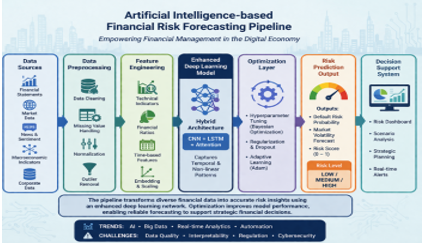

The rapid expansion of the digital economy has transformed the financial landscape, compelling publicly listed companies to adopt advanced technologies for effective risk forecasting and management. Traditional statistical approaches often fail to capture nonlinear dependencies and high-dimensional relationships inherent in financial data, leading to suboptimal forecasting performance. In this context, artificial intelligence techniques, particularly deep learning models, have emerged as powerful tools capable of modeling complex temporal and structural patterns. This study presents a comprehensive review of artificial intelligence techniques for financial risk forecasting, emphasizing the integration of enhanced deep learning networks within digital financial ecosystems. The paper explores the evolution of machine learning and deep learning approaches, including recurrent neural networks, convolutional neural networks, and hybrid optimization-based architectures, highlighting their applications in predicting market volatility, credit risk, and operational uncertainties. Furthermore, the study examines the role of big data analytics, real-time processing, and digital transformation in improving forecasting accuracy. Key challenges such as model interpretability, data heterogeneity, overfitting, and regulatory constraints are critically analyzed. The findings indicate that enhanced deep learning frameworks, when combined with optimization techniques, significantly improve prediction accuracy and robustness. The paper concludes by identifying emerging research directions and practical implications for financial institutions aiming to leverage artificial intelligence for strategic decision-making and risk mitigation.